Consolidating biosecurity and raw material costs, together with openness to exploring new markets, are the main challenges facing the global broiler industry in the second half of 2025

This highly regarded quarterly report by RaboResearch on the global poultry industry for Q3 2025, authored by Nan-Dirk Mulder and his team and published on 26 June 2025, provides a detailed overview of the market. It examines how geopolitical tensions, such as the Israel–Iran conflict and the import tariffs proposed by the United States, together with avian influenza outbreaks in key regions including the United States, Europe and Brazil, are shaping industry dynamics.

The document, summarised below in this NeXusAvicultura article, analyses supply and demand trends, feed prices and implications for global trade, highlighting uncertainties despite robust underlying demand. Finally, it provides regional analyses for Europe, the United States, Mexico, Brazil, South Africa, China, Japan and Thailand, indicating how these global factors are impacting their respective local markets.

Global poultry outlook for Q3 2025: between geopolitical uncertainty and avian influenza — where is the sector headed?

The global poultry sector has navigated a relatively bullish first half of 2025. However, the outlook for the second half is marked by growing volatility and uncertainty, driven primarily by two dominant realities: geopolitical tensions and avian influenza outbreaks. Although the fundamentals of the global poultry market remain solid, supported by elevated beef and egg prices and stability in feed costs, the landscape demands constant vigilance from industry professionals.

Geopolitical headwinds: tariffs and armed conflicts

Geopolitical tensions are a significant factor influencing the global economy and, consequently, poultry markets. The International Monetary Fund (IMF) has already downgraded its global GDP growth forecast by 0.5% due to this economic uncertainty.

- US import tariffs: The prospect of a trade war remains latent following the announcement (and subsequent postponement) of significant US tariffs in April. Should bilateral trade agreements be reached, the US poultry sector could gain greater market access, potentially at the expense of domestic producers or competing exporters. On the other hand, a prolonged trade war could restrict US producers’ market access, benefiting other exporters such as Brazil, Thailand, Russia and the EU. This scenario could lead to price inflation, with a disproportionate impact on economies facing the highest tariffs, particularly in Asia and Africa.

- Israel–Iran conflict: A potential escalation of the Middle East conflict could add a further layer of uncertainty. This region is a key poultry import market, accounting for approximately 20% of global poultry trade and 90% of global whole chicken trade. A blockade of the Strait of Hormuz, for example, would affect trade with Iraq, Kuwait, the United Arab Emirates and Bahrain, in addition to triggering a significant rise in oil prices.

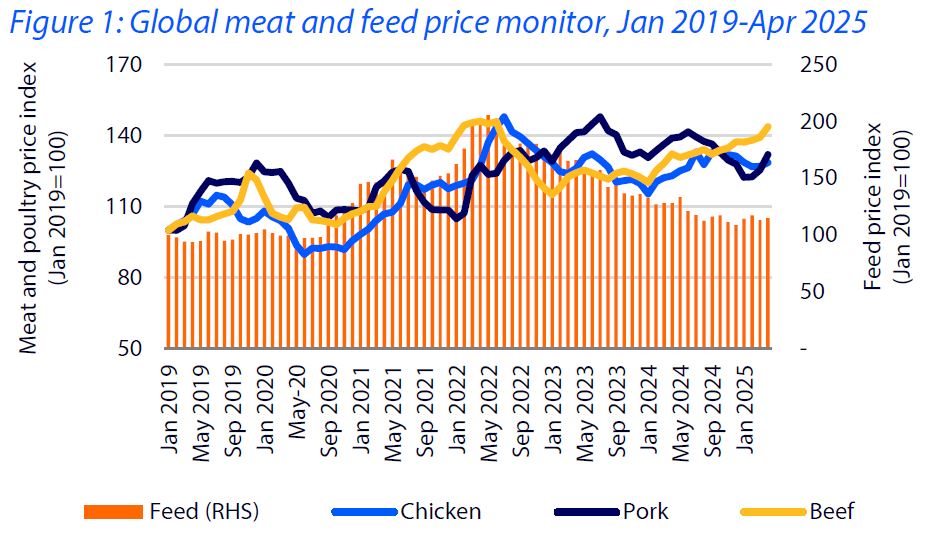

Price tracking of major meat categories and raw material costs at global level. Source: Global poultry quarterly Q3 2025: Geopolitics and bird flu to shape the 2025/26 poultry outlook. RaboResearch report, 26 June 2025

The dependence of feed commodity and ingredient markets on a small number of countries also exposes the sector to sudden short-term volatility and disruptions in the event of trade tensions. Although the feed price outlook remains stable under the baseline scenario, the introduction of tariffs or restrictions on US soybean and/or maize trade by importing countries could trigger significant shifts in trade flows, with Brazil as a potential beneficiary, and a likely rise in domestic feed prices.

The “Sword of Damocles” of the persistent avian influenza threat

Avian influenza outbreaks continue to be a major source of disruption in global markets. Currently, Europe, the US and Brazil are all affected, with growing risk in the Southern Hemisphere as winter approaches.

- Global and regional impact: The wave of outbreaks has shaken global trade dynamics.

- Brazil: The outbreak in Rio Grande do Sul has dealt a major blow to global trade, given Brazil’s dominance as an exporter. Approximately 40% of Brazilian exports remain blocked by key importers, including China, the EU, South Africa, Mexico and the Philippines. This has inevitably led to short-term oversupply in the domestic market and downward pressure on broiler meat prices in major consuming regions for the Brazilian poultry industry.

- USA: Outbreaks, with more than 40 million cases this year, have significantly affected the egg industry, driving prices to all-time highs in the first quarter. Exposure through wild birds and the dairy industry — a source of new cases — remains a primary risk.

- Europe: A wave of cases in March and April affected the poultry industry in Central Europe (Poland, Hungary, northern Italy), pushing chicken, duck and egg prices to record levels. The situation in breeder flocks in Poland poses an additional challenge, as the supply of hatching eggs was already very tight. Rebuilding the EU poultry supply is expected to be a slow process, keeping markets tight until at least Q4 2025.

- Hatching egg trade: This segment has also been severely affected globally, posing a challenge for countries dependent on hatching egg imports, particularly in the Middle East, Africa and Latin America.

For the Brazilian poultry industry, the avian influenza outbreak of 16 May, now closed, has been an unprecedented major shock, and the risk of new outbreaks will persist throughout the Southern Hemisphere winter. As Brazil recovers, alternative exporters such as Thailand, Russia and the USA will benefit.

Forecasts revise global broiler production growth down to 2%–2.5%

Despite the uncertainties, the current fundamental conditions of the global market remain positive for the poultry industry. Global production is projected to grow by 2% to 2.5% in 2025, a figure revised downward from the initial 3% to 2.5% forecast, owing to economic uncertainty and avian influenza outbreaks.

The regional production and consumption outlook is as follows:

- United States: Chicken prices remain strong, driven by robust foodservice demand and a constrained supply. Despite strong margins, supply growth is limited by productivity challenges and a reduced availability of breeders. The avian influenza situation in Brazil is considered a moderately positive factor for US exports for the remainder of the year.

- Mexico: Live chicken prices have reached all-time highs due to health challenges, extreme heat and restrictions on imports from Brazil, all of which have curtailed production. Imports surged sharply in early 2025, with Brazil gaining a significant market share prior to the temporary ban. Imports are expected to remain elevated to combat food price inflation.

- China: Chicken prices remain under pressure due to sluggish demand and rising domestic production. Although grandparent stock (GPS) imports declined, current inventory levels are sufficient. The ban on Brazilian poultry imports has created uncertainty, particularly regarding the prices of specific cuts such as wings and feet. Total poultry imports are expected to decline in 2025, as no alternative supplier can offer volumes equivalent to those previously sourced from Brazil. Chinese exports, however, increased considerably.

- Thailand: Thailand is positioning itself as a key alternative poultry source while Brazilian exports remain restricted. Both domestic and international demand are strong, and total exports reached a record high in Q1. The industry is benefiting from robust export performance and its competitive position relative to more expensive pork and beef.

- Japan: Demand for affordable chicken remains strong amid food price inflation. Chicken import volumes are expected to increase year-on-year in Q3. Revised sanitary conditions for imports from Brazil could allow Japan to import more Brazilian chicken at lower prices, given that other countries have suspended imports.

- South Africa: Chicken demand is strong, with frozen chicken prices on the rise. However, the suspension of poultry imports from Brazil — which accounted for 85% of South Africa’s imports in Q1 2025 — will have a significant impact, particularly on the mechanically deboned meat (MDM) market. This creates opportunities for domestic producers and alternative exporters such as Argentina, Spain, Ireland and Thailand.

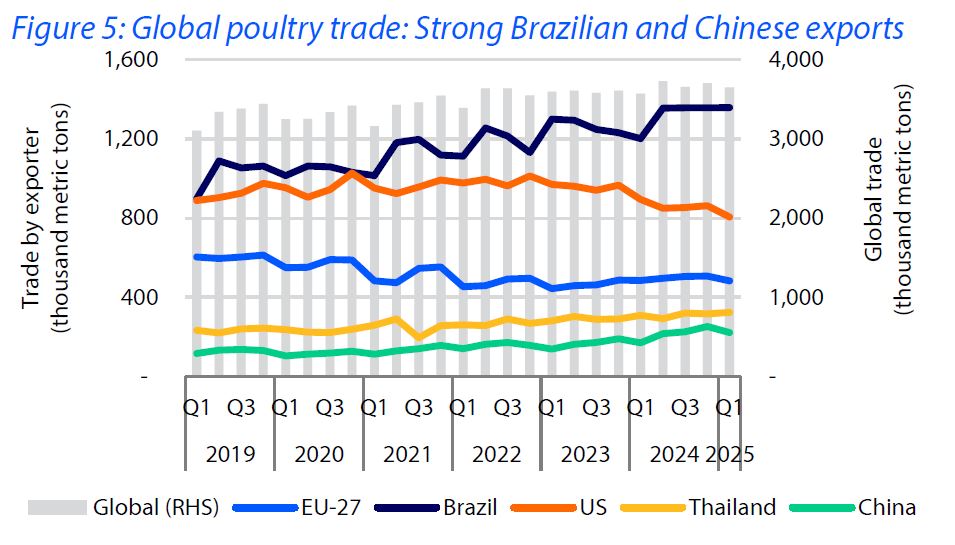

Trends in global chicken trade. Source: Global poultry quarterly Q3 2025: Geopolitics and bird flu to shape the 2025/26 poultry outlook. RaboResearch report, 26 June 2025

Conclusion: adaptability, or “Be water, my friend”

The poultry outlook for the remainder of 2025, and possibly into 2026, will be one of solid production and demand fundamentals combined with significant volatility. The capacity to adapt and the agility to respond to shifts in trade flows and animal health-related disruptions will be critical for industry professionals. Maintaining strict biosecurity, diversifying supply sources and exploring new markets will be fundamental strategies for mitigating risks and capitalising on the opportunities that arise in this dynamic global environment.

About Rabobank

Rabobank Group is a global financial services leader offering wholesale and retail banking, leasing and real estate services in more than 38 countries worldwide. Founded more than a century ago, Rabobank is today one of the world’s largest banks with over USD 660 billion in assets. In the Americas, Rabobank Wholesale Banking North America is a premier corporate and investment bank for the food, agribusiness, commodities and energy industries.

About RaboResearch Food & Agribusiness

RaboResearch Food & Agribusiness has 85 analysts working in local teams across Rabobank’s global network. They generate knowledge and develop views and perspectives on businesses, topics and developments in the food and agribusiness sectors worldwide. All analysts have their own sectoral specialisations, ranging from meat and fish to dairy, vegetables, fruit and floriculture, coffee and cocoa.

Source:

Nan Dirk Mulder, RABOBANK

-. Press release: RABOBANK Report [26-June-2025]

Further reading:

-. 2025 broiler industry map: key trends