Amid economic uncertainty and high prices for other meats, global poultry production will grow in 2025, albeit at a slower pace, with poultry meat and eggs firmly establishing themselves as the affordable nutritional option preferred by the world’s population

Overview of Global Food Markets

The extensive figures and statistics recently published (June) in the “FAO Food Outlook 2025” report present a relatively optimistic outlook for food commodity markets, anticipating an increase in production across all commodities except sugar. However, this growth trend will have varying impacts on stock recovery, depending on the balance between supply and demand. Global food production remains vulnerable to weather conditions, and geopolitical tensions, policy uncertainty and potential retaliatory measures could adversely affect trade prospects. The report is published against a backdrop of growing economic uncertainty; although the global economy appeared to stabilise at the start of 2025, the outlook has since shifted, making the global growth profile more fragile.

Global cereal production (including rice in milled equivalent) is projected to reach a record 2,911 million tonnes in 2025, surpassing 2024 production by 2.1 per cent. Production of all major cereals is expected to increase, with the largest rise forecast for maize and the smallest for wheat. Cereal prices in May 2025 averaged 109.0 points, 8.2 per cent lower than in 2024.

Global poultry meat production: the fastest-growing meat sector by far

If we analyse in depth the section of this biannual report (published each year in June and November) focusing on market assessments, we can see that the “FAO Food Outlook” of June 2025 provides a detailed analysis of the global situation and outlook for meat and meat products.

International meat prices

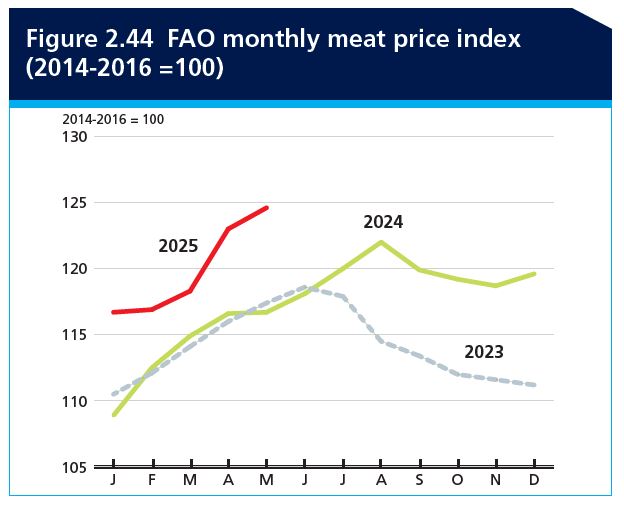

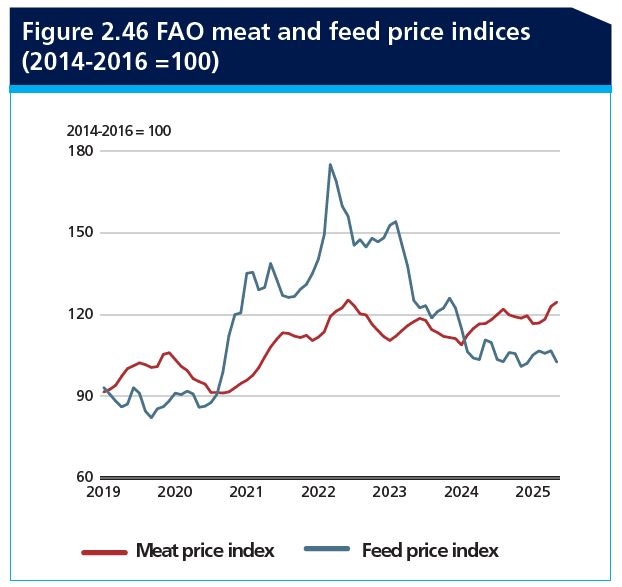

The FAO Meat Price Index (MPI) has shown an upward trend during the first five months of 2025, reflecting the reduction in exportable supplies in several major producing countries, combined with sustained global demand. Market uncertainty, driven by widespread animal disease outbreaks and trade policy tensions, has contributed to rising prices. Additionally, anticipatory stockpiling by some importing countries, fearing potential trade disruptions, has exerted further upward pressure on international meat prices. In May 2025, the MPI averaged 124.6 points, 6.8 per cent higher than in January and 6.8 per cent above the corresponding value from the previous year.

Poultry meat: production up 1.7%, prices down 0.7%

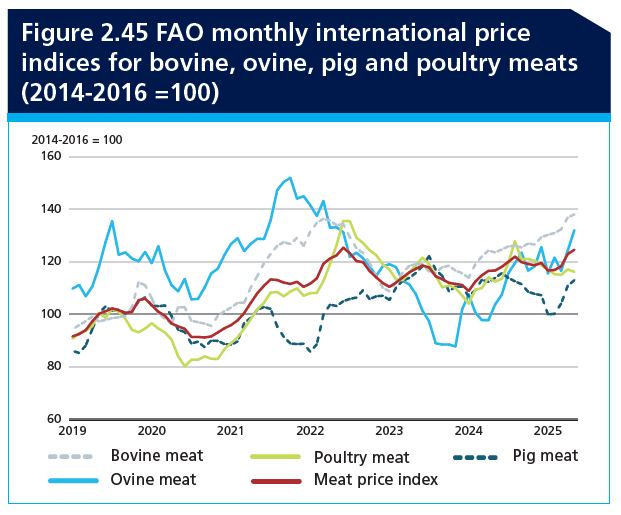

Sheepmeat prices rose by 16.4 per cent, pigmeat prices by 13.6 per cent and bovine meat prices by 6.1 per cent between January and May 2025. In contrast, the poultry meat price index declined slightly, by 0.7 per cent.

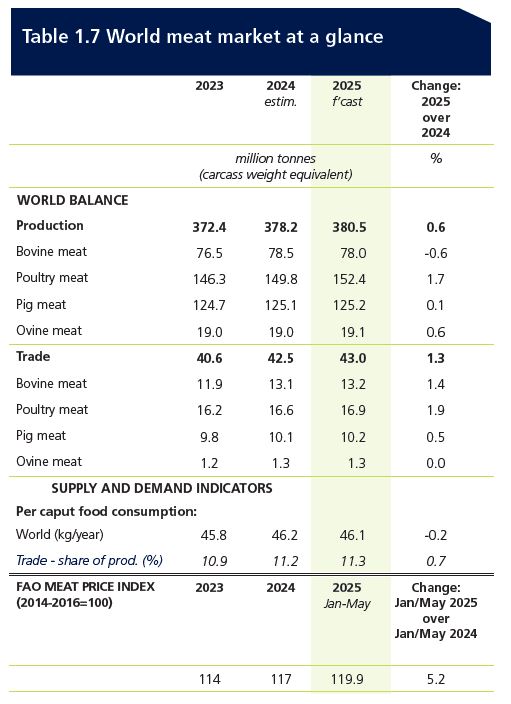

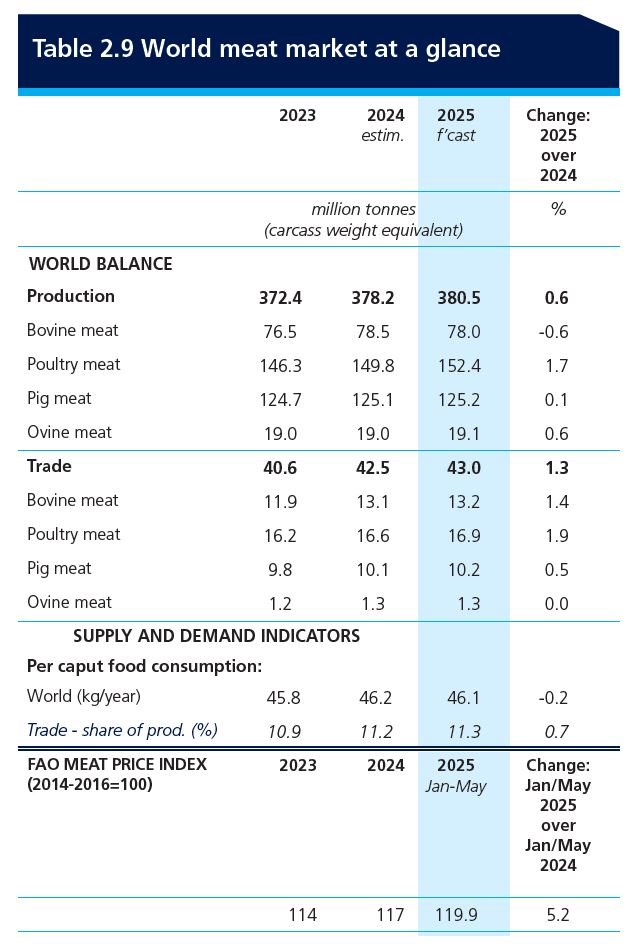

Table. World Meat Market at a Glance (change: 2025 over 2024):

| Category | 2024 (Estimated) (million tonnes) | 2025 (Forecast) (million tonnes) | Change (%) |

|---|---|---|---|

| WORLD BALANCE | |||

| Total production | 378.2 | 380.5 | +0.6% |

| – Bovine meat | 78.5 | 78.0 | -0.6% |

| – Poultry meat | 149.8 | 152.4 | +1.7% |

| – Pigmeat | 125.1 | 125.2 | +0.1% |

| – Ovine meat | 19.0 | 19.1 | +0.6% |

Total trade | 42.5 | 43.0 | +1.3% |

| – Bovine meat | 13.1 | 13.2 | +1.4% |

| – Poultry meat | 16.6 | 16.9 | +1.9% |

| – Pigmeat | 10.1 | 10.2 | +0.5% |

| – Ovine meat | 1.3 | 1.3 | 0.0% |

| SUPPLY AND DEMAND INDICATORS | |||

| Food consumption per capita: World | 46.2 (kg/year) | 46.1 (kg/year) | -0.2% |

| Trade – % of production | 11.2% | 11.3% | +0.7% |

| FAO MEAT PRICE INDEX (2014-2016=100) | |||

| 2024 (January–May) | 117 | 119.9 (January–May 2025) | +5.2% |

Global meat production in 2025

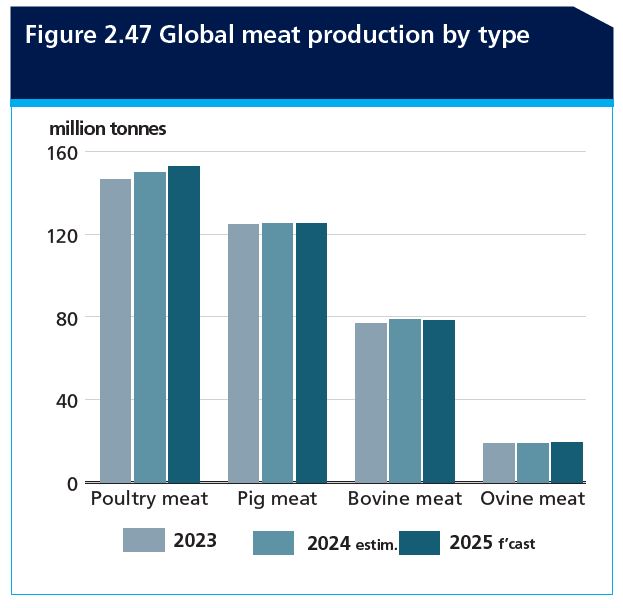

Global meat production is forecast to increase modestly in 2025, by 0.6 per cent year-on-year, to reach 380 million tonnes (carcass weight equivalent). This growth will be driven primarily by the expected expansion of poultry meat production, while pigmeat and ovine meat production will register only marginal increases. In contrast, bovine meat production is forecast to decline, partially offsetting overall growth.

Poultry meat production is projected to continue expanding steadily, supported by sustained consumer demand owing to its relative affordability, particularly in a context of constrained household purchasing power. Despite ongoing outbreaks of highly pathogenic avian influenza (HPAI) in several key regions and persistent limitations in breeder flock availability, favourable operating margins are expected to sustain production growth.

Global meat trade in 2025

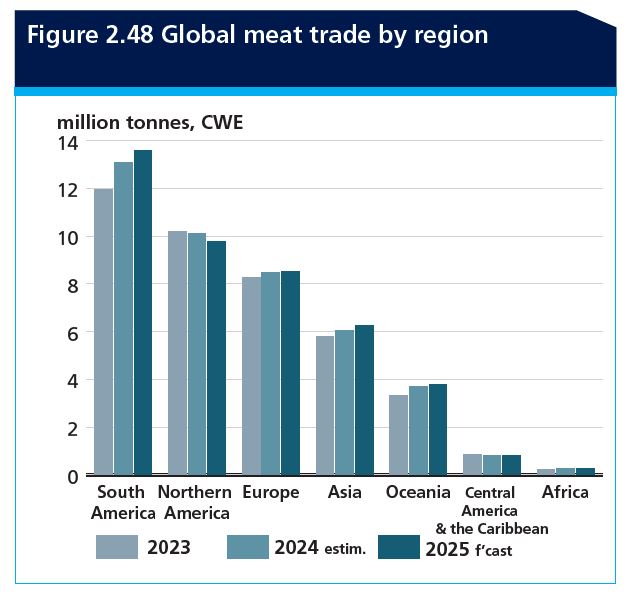

Global meat trade is forecast to grow by 1.3 per cent in 2025, reaching 43 million tonnes, representing a significant slowdown compared with the estimated 4.7 per cent growth in 2024. The modest projected growth is underpinned by expectations of a tighter global supply and firm import demand. However, growth will likely be affected by geopolitical tensions, the implementation of trade-restrictive measures and the continued spread of animal diseases, which could continue to disrupt trade flows. The projected trade expansion will be driven primarily by higher poultry meat shipments, supported by its affordability relative to other meats.

Domestic demand and global trade will drive poultry meat production to a new record in 2025, surpassing 152 million tonnes

Global poultry meat production is projected to reach 152.4 million tonnes in 2025, a year-on-year increase of 1.7 per cent. This growth is driven by stable input costs, firm global demand and the continued price competitiveness of poultry meat compared with other animal protein sources, particularly in a context of limited supply of alternative meats.

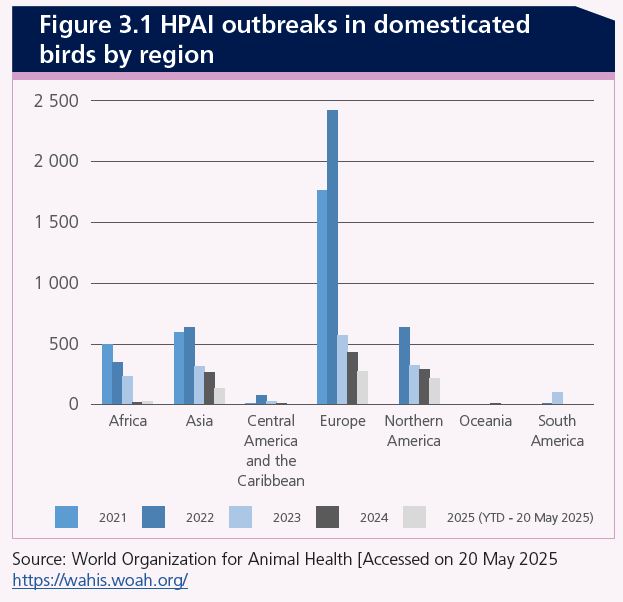

Nevertheless, production growth could be constrained in some regions by persistent animal disease outbreaks (notably HPAI and Newcastle disease) and breeder flock shortages. Notable production increases are anticipated in Brazil, China, the European Union and the United States, as well as in India, Indonesia, Mexico, Pakistan, the Russian Federation and Turkey, driven by sustained domestic and export demand.

Regarding trade, global poultry meat trade is forecast to reach 16.9 million tonnes in 2025, an increase of 1.9 per cent over the previous year. This growth is expected to be driven largely by increased import demand in key markets, although it will be partially offset by lower purchases from China.

Despite a slight easing of restrictions, Chinese imports will likely be affected by a combination of weak demand, domestic market oversupply, trade tensions and disease-related import bans.

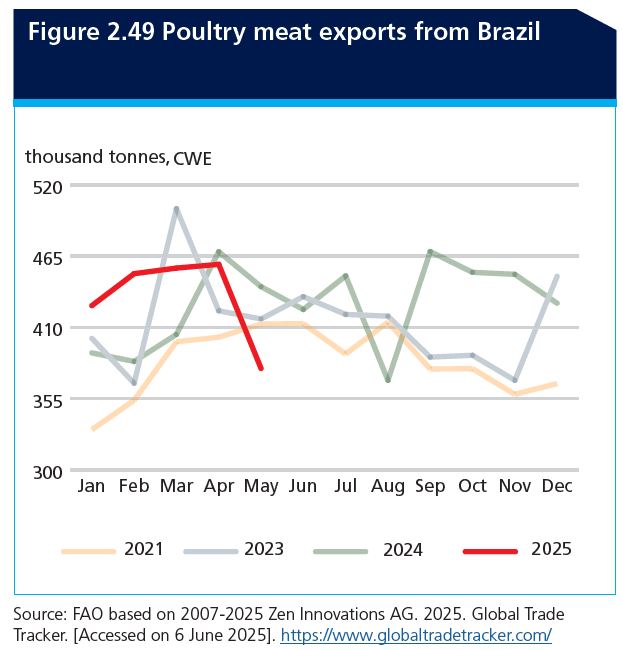

The projected increase in global demand is expected to be met by greater export availabilities from Brazil, the European Union, Thailand and Turkey. However, the recent detection of HPAI on a commercial farm in Brazil could temporarily restrict its exports to some destinations. In contrast, deliveries from the United States are anticipated to decline, constrained by reduced price competitiveness and HPAI-related trade restrictions.

How severely has Highly Pathogenic Avian Influenza (HPAI) impacted broiler and layer production?

HPAI is a viral disease affecting domestic and wild bird populations, and its cross-border spread has become more persistent and year-round since 2020. Although the broiler sector has been less affected owing to its shorter production cycles and enclosed housing systems, the laying hen sector has experienced more pronounced and prolonged disruptions. Food safety is not the primary concern, as the virus is inactivated at standard cooking temperatures. However, its economic impact is significant, disrupting supply chains, eroding farm margins and triggering international trade restrictions.

Impact on Eggs: Fresh (table) eggs are produced and consumed primarily in domestic markets, which limits global trade due to their short shelf life, fragility and differences in food safety standards. This makes domestic markets highly sensitive to local supply disruptions. In the United States, during the winter season of 2024–2025, retail egg prices rose sharply following a major HPAI outbreak. Average prices for Grade A large eggs increased by 13.6 per cent in December 2024, followed by 19.5 per cent in January and 19.1 per cent in February 2025. By March 2025, prices were 108 per cent higher than the previous year, driven largely by the culling of 41 million laying hens at the peak of the outbreak. In response, the USDA implemented support measures, including financial assistance, biosecurity investments, vaccine research and the exploration of temporary import options.

Globally, hen egg production has grown steadily, reaching 91 million tonnes in 2023 (approximately 1.7 trillion eggs), with an additional 6 million tonnes from other poultry species. International egg trade volumes remained modest in 2022 and 2023 (2.2 million tonnes), but rose sharply to 4 million tonnes in 2024, driven largely by a fourfold increase in exports from the Netherlands, potentially reflecting re-export activity.

In 2023, China accounted for 37 per cent of global egg production, followed by the United States and India, which contributed approximately 7 and 8 per cent, respectively.

What are the 5 key trends in global poultry production revealed by this FAO report?

- Sustained growth driven by affordability: Poultry meat production and trade continue to expand globally, underpinned by steady consumer demand owing to its relative availability and affordability compared with other meats and favourable operating margins.

- Critical impact of Highly Pathogenic Avian Influenza (HPAI): HPAI remains a significant biological threat, particularly for the laying hen sector, causing massive flock depletions and sharp price increases, as observed in the US egg market. Temporary outbreaks also affect poultry meat trade.

- Strengthened biosecurity and preventive vaccination: The persistence of HPAI has driven the implementation of integrated management strategies, including enhanced biosecurity, disease surveillance and vaccination campaigns, although uptake of the latter varies globally due to trade-related concerns.

- Shifts in trade flows and regionalisation: Temporary trade restrictions imposed by importing countries due to animal disease outbreaks are reshaping global trade patterns. This encourages diversification of sources and regionalisation agreements to mitigate disruptions.

- Price volatility and macroeconomic factors: While animal disease outbreaks and trade tensions influence prices, broader macroeconomic factors such as feed and energy costs, as well as general economic uncertainty, also contribute to price volatility in poultry markets.

Federico Castelló, Founder of NeXusAvicultura

For further reading:

-. “FAO Food Outlook” June 2025 report (152 pages)

-. Other in-depth articles published on NeXusAvicultura on global poultry trade