Poultry meat consolidated its role in 2024 as the growth engine of the global meat market, against a backdrop of rising prices and recovery in global trade.

Overview of the Global Meat Market in 2024

In 2024, poultry meat consolidated its position as the primary growth driver of the global meat market, in a context of trade recovery and a modest rise in prices. According to the report “Meat Market Review: Overview of global market developments in 2024” published by the FAO in April 2025, poultry meat production and trade grew strongly, driven by lower feed costs and consumer preference for more affordable animal proteins.

General Overview 2024

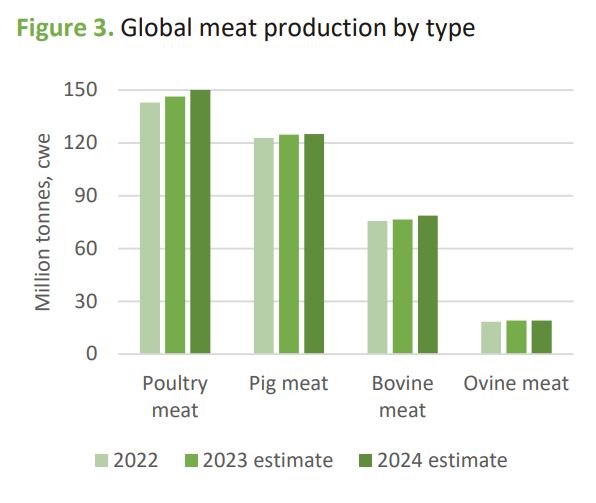

- Global meat production increased by 1.7% in 2024, reaching 379 million tonnes carcass weight equivalent, driven primarily by poultry meat.

- Global meat trade rebounded by 4.7%, reaching 42.5 million tonnes, reversing two years of decline, underpinned by improved economic conditions and the easing of certain trade barriers.

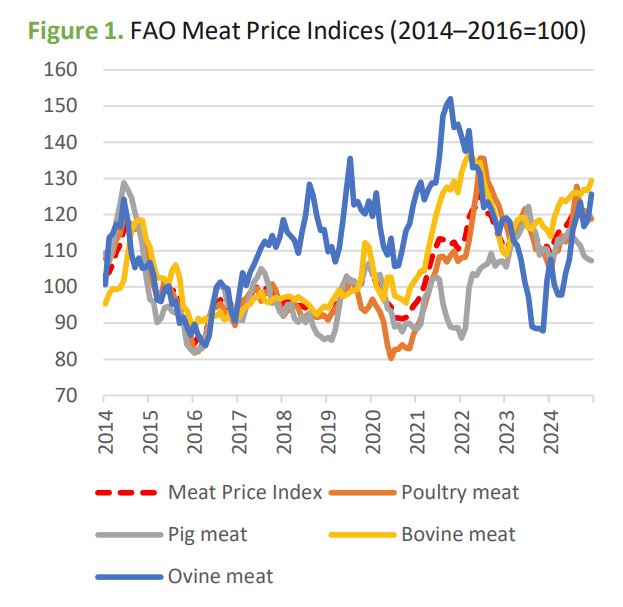

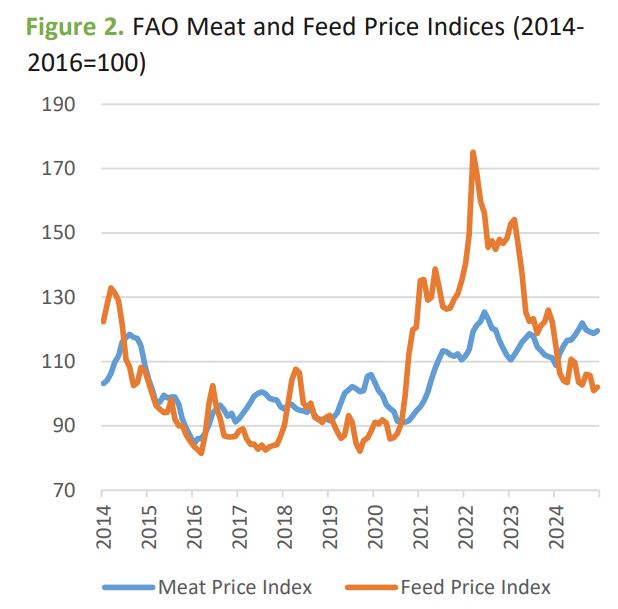

- The FAO Meat Price Index rose by 2.8% in 2024; ovine meat prices recorded the strongest increase (9.1%), followed by bovine (6.7%) and poultry (1.5%), while pigmeat fell by 2.0%.

Table 1. Global production trends by meat type in 2024

| Meat type | Global production 2024 (Mt cwe) | Production change 2024 | Key trade feature | Price trend |

|---|---|---|---|---|

| Poultry | 150.1 | +2.6% | Trade +2.3%, to 16.6 Mt | +1.5% on FAO index |

| Bovine | 78.7 | +2.8% | Trade +9.8%, to 13.1 Mt | +6.7% |

| Pigmeat | 125.1 | Stable | Trade +3.0%, to 10.1 Mt | −2.0% |

| Ovine | 19.1 | +0.6% | Exports +7.5%, to 1.3 Mt | +9.1% |

Poultry meat: production, key countries and health challenges

Global poultry meat production (chicken, turkey, duck, etc.) reached 150 million tonnes in 2024, a 2.6% increase over 2023, making it the segment contributing most to total meat output growth. The upturn was driven by lower feed and energy costs, alongside robust global demand that maintained attractive prices and margins, despite the persistent presence of highly pathogenic avian influenza (HPAI) in several regions.

NeXusAvicultura Note:

Non-specialist publications frequently make a statistical error by conflating “poultry meat” with “chicken meat”, often as a result of inaccurate translations.

In this specific case, when global poultry meat production is reported as 150 million tonnes in 2024, this figure encompasses chicken alongside turkey, duck, goose, cut-up hen meat and all other types of meat from any species of poultry.

Although not mentioned in the FAO report, production of broiler chicken meat alone in 2024 was approximately 100 million tonnes worldwide. The remainder, up to the 150 million tonne total, comprises other poultry meat types other than broiler chicken.

- The four major producers (China, the United States, Brazil and the European Union) all increased their production.

- China increased its poultry production by 3.8%, driven by falling soybean and maize prices, which stimulated both large and small producers, particularly of white broilers.

- However, in China, weak domestic demand combined with a strong expansion in supply led to price declines, generating oversupply and financial losses for many producers.

- In the United States, the production increase was supported by higher slaughter rates and heavier slaughter weights, which offset losses from HPAI-affected broilers.

- Brazil increased production despite severe flooding in May 2024 and a Newcastle disease outbreak in July in Rio Grande do Sul, underpinned by lower feed costs and strong domestic and external demand.

- The European Union also raised its output, driven by lower feed costs, greater demand for affordable protein, reduced HPAI incidence, and a geographical shift of production away from the northwest towards less-affected areas.

- Beyond these leading producers, notable increases were recorded in Turkey, Pakistan, India, Russia, Egypt, South Africa and Mexico, all following the same pattern: strong demand for a relatively low-cost protein.

Table 2. Poultry meat production by region (2023–2024)

| Region | Production 2023 (thousand t cwe) | Production 2024 (thousand t cwe) | Comment |

|---|---|---|---|

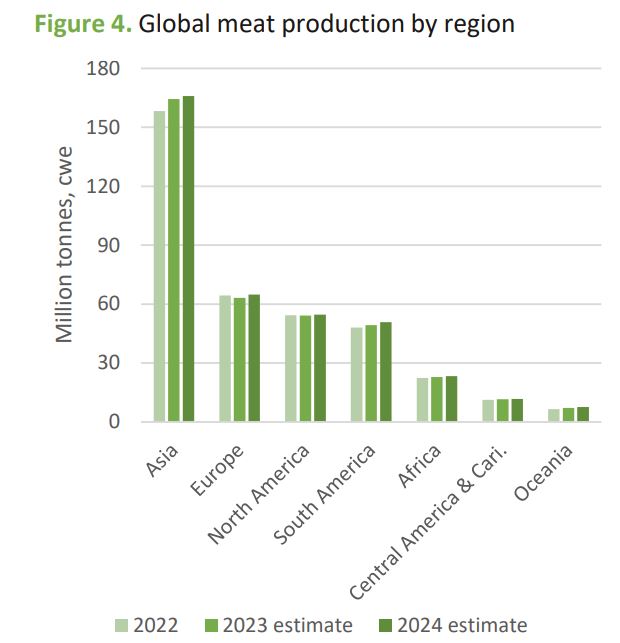

| Asia | 58,760 | 60,488 | Growth centred on China, India and South-East Asia. |

| Africa | 7,953 | 8,231 | Increase linked to higher urban consumption. |

| Central America and Caribbean | 6,007 | 6,184 | Mexico accounts for a large share of the increase. |

| South America | 23,432 | 23,902 | Brazil dominates regional growth. |

| North America | 25,436 | 25,736 | United States maintains high volumes. |

| Europe | 23,047 | 23,770 | European Union and Russia as the main drivers. |

| Oceania | 1,697 | 1,760 | Moderate growth. |

| World | 146,332 | 150,070 | +2.6% year-on-year. |

Global poultry meat trade: realignment of flows and leadership of Brazil and China

Global trade in poultry meat reached 16.6 million tonnes in 2024, 2.3% more than in 2023, reversing the previous year’s decline. The increase was driven by a recovery in import demand, accompanied by higher shipments from China, Brazil, the European Union and Thailand, while the United States and Turkey reduced their exports.

Exporters

- China: its poultry meat exports grew by approximately 34% year-on-year, driven by strong demand for processed chicken products in Japan, the European Union and the United Kingdom.

- The improvement in relative prices allowed China to gain market share against traditional exporters such as Thailand in the processed segment.

- Brazil consolidated its position as the world’s leading exporter, with a 3% increase in its shipments, despite a voluntary suspension of exports in July following a Newcastle disease outbreak in Rio Grande do Sul.

- The rapid resumption of trade flows was facilitated by a regionalisation approach adopted by many importing countries, which confined restrictions solely to the affected region.

- Reduced purchases by China were offset by higher shipments to the United Arab Emirates, Japan, the Philippines, Mexico and Iraq.

- The European Union increased its exports in 2024, supported by growing demand from African markets.

- Thailand increased its shipments on the back of ample exportable supply and stronger demand for processed chicken.

- The United States reduced its exports by 9% due to dollar appreciation and domestic supply constraints caused by HPAI; while sales to Mexico increased, shipments to China, Cuba, the Philippines and Guatemala declined.

- Turkey recorded its second consecutive year of export decline; following the disruptions of 2023 caused by HPAI and trade bans, the country imposed an export quota between May and December 2024 to contain domestic prices, further curbing volumes available for export.

Importers

- Demand increased in Vietnam, Japan, the United Kingdom, the United Arab Emirates and the Philippines, driven by insufficient domestic supply and strong consumer demand.

- China reduced its poultry meat imports by 17%, reflecting domestic oversupply; purchases declined from all major suppliers except the Russian Federation, which became its third-largest supplier with an increase of approximately 6%.

- Korea also cut imports following the normalisation of its domestic supply and the expiry in March 2024 of the emergency tariff-rate quota that had reduced the cost of purchases the previous year.

Table 3. Key poultry meat trade dynamics in 2024

| Actor | Role | 2024 performance | Key factor |

|---|---|---|---|

| Brazil | Largest exporter | Exports +3% | Regionalisation in response to Newcastle disease, diversification of destinations. |

| China | Major producer and emerging exporter | Exports +34%, imports −17% | Domestic oversupply and competitiveness in processed products. |

| European Union | Significant exporter | Shipments up, particularly to Africa. | Lower HPAI incidence and geographical reallocation of production. |

| United States | Traditional exporter | Exports −9% | Strong dollar and HPAI-related supply constraints. |

| Turkey | Regional exporter | Decline for the second year | Export quotas to contain domestic prices. |

Other meats: bovine, pigmeat and ovine

Although poultry meat leads overall growth, the report highlights significant dynamics in the other categories, with implications for the global balance of animal proteins.

Bovine

- Global bovine meat production: 78.7 million tonnes, +2.8%, driven by Brazil, Australia, China, the European Union and India; declines recorded in Argentina and New Zealand.

- Growth linked to greater slaughter availability (heifer culling, destocking) and strong international demand, particularly from the United States.

- Bovine meat trade increased by 9.8% to 13.1 million tonnes, with the United States, China and Iran as the main demand drivers.

- Brazil and Australia posted strong export increases, supported by low production costs, depreciated currencies and market diversification strategies.

Pigmeat

- Global production was virtually stable, at around 125.1 million tonnes, with declines in China, the Philippines, Canada and Japan, and increases in the European Union, the United States, the Russian Federation and Viet Nam.

- In China, production fell by 1.5% due to sow herd reductions, weak demand and financial uncertainty among producers.

- Global pigmeat trade increased by 3.0% to 10.1 million tonnes, driven by higher imports from Mexico, the Philippines, the Republic of Korea and Japan.

- China, the world’s largest importer, significantly reduced its purchases due to weak domestic consumption, despite an anti-dumping investigation into imports from the European Union which had not yet had a material impact on volumes in 2024.

- The United States and Brazil increased exports, supported by ample supply and competitive prices, while the European Union reduced its shipments due to lower demand from the United Kingdom and China, partially offset by other Asian destinations.

Ovine

- Global ovine meat production: 19.1 million tonnes, +0.6%, with increases in India, Türkiye, Australia and Pakistan, and declines in China, the European Union, the United Kingdom and New Zealand.

- Ovine meat trade recorded the strongest relative growth: global exports +7.5% to 1.3 million tonnes, driven by the United States, the United Kingdom and Near East countries, with China reducing its purchases.

- Australia accounted for 52% of global exports and increased its shipments by 17%, offsetting weaker Chinese demand with sales to the United States, Asia, the Middle East and the United Kingdom.

Overall, the report confirms poultry meat as the most dynamic meat protein, by virtue of its competitive production costs, strong demand and capacity for rapid adjustment, while bovine and ovine meats benefit from solid international demand and pigmeat navigates a rebalancing phase shaped by adjustment in China and new opportunities in the Americas and Asia.

Source:

-. Report “Meat Market Review: Overview of global market developments in 2024” published by the FAO in April 2025.

Further reading:

-. Other in-depth articles published on NeXusAvicultura on global poultry trade