This report, prepared by the NeXusAvicultura team, offers a comprehensive analysis of Brazil’s dominance in global poultry meat exports to Europe during the 2023–2025 cycle. Driven by macroeconomic advantages and low production costs, the Brazilian agri-food industry has managed to navigate EU sanitary requirements and European protectionism by prioritising the sale of premium cuts and processed preparations. The report also details how the post-Brexit UK market has significantly increased its dependence on high-value-added Brazilian poultry products.

On the sanitary front, the document examines Brazil’s successful management of the Avian Influenza (HPAI) outbreak of May 2025 through sanitary regionalisation strategies. However, the analysis warns of an imminent trade rupture in 2026: the European Union’s decision of 12 May 2026 to exclude Brazilian meats on the basis of antimicrobial regulations. This blockade, strongly linked to geopolitical tensions surrounding the Mercosur Agreement, could halt or very substantially reduce Brazilian poultry meat exports to the EU and, if Europe does not yield ground, will demand an unprecedented structural overhaul of the poultry production model for the South American agri-food sector.

Comprehensive analysis of Brazilian poultry meat exports to Europe (2023–2025) and possible scenarios should the 12 May 2026 ban ultimately take effect. Trade dynamics, sanitary barriers and geopolitical reconfiguration

1. Macroeconomic foundations and the structural dominance of the Brazilian poultry industry

The architecture of global animal protein trade is undergoing a phase of profound structural reconfiguration, and at the absolute epicentre of this transformation stands the Brazilian agri-food industry. In order to rigorously analyse, with mathematical and analytical precision, the trade flows of poultry meat exports to the European continent during the 2023–2025 triennium, it is methodologically essential to first dissect the macroeconomic, productive and competitiveness foundations that have underpinned Brazil’s dominant position in the global market. The South American nation does not merely operate as one more supplier on the international stage; it acts as the principal architect of price, volume and supply dynamics, dictating trends in avian protein at a global level.

According to consolidated metrics from the United States Department of Agriculture (USDA) and the Brazilian Animal Protein Association (ABPA), Brazil holds the title of the world’s third-largest producer of chicken meat, surpassed only by the United States of America and the People’s Republic of China, while undisputedly maintaining first place as the world’s largest exporter of this protein. Global market projections and analyses indicate that the Brazilian poultry industry accounts for approximately 35% to 36% of all global chicken meat exports. This monumental market share, which leaves its closest competitors — the European Union and the United States — far behind, is not the result of short-term statistical anomalies, but rather the culmination of decades of massive vertical integration, military-grade biosecurity adoption in its facilities, and an aggressive trade insertion policy.

Throughout the analysed cycle (2023–2025), Brazil’s productive capacity has displayed extraordinary resilience, driven by both external demand and adjustments in domestic consumption. Official figures indicate that national production exceeded 14.97 million tonnes in 2024, rising to 15.289 million metric tonnes by the close of 2025. Industry estimates forecast that this upward trajectory will continue, projecting a record production volume of 15.8 million metric tonnes for 2026, which would represent an additional year-on-year increase of 3%. In parallel, the Brazilian domestic market exhibits one of the highest per capita consumption rates on the planet, absorbing 46.7 kilograms per inhabitant per year. This domestic consumption base provides producers with an invaluable financial cushion, absorbing lower-value cuts or non-exportable surpluses, which allows corporations to concentrate the export of premium, high-value-added cuts — such as breast meat — on high-purchasing-power markets like Europe.

1.1. Exchange rate determinants and production costs

The underlying engine driving this hypercompetitiveness in international markets — and making Brazilian products economically irresistible to European importers — is a convergence of endogenous macroeconomic factors. In the first instance, the structural abundance and low cost of key animal feed inputs — particularly soya and maize — provide the Brazilian production chain with a protective shield against the extreme volatility of international grain markets. This intrinsic advantage in the production cost structure proves to be an insurmountable barrier to entry for European poultry producers, who are structurally dependent on the mass importation of these very same South American or North American grains to formulate the feed for their own flocks.

In the second instance, and even more decisively for export flows, monetary policy and exchange rate fluctuations have acted as a de facto structural subsidy for Brazilian exporting corporations. The local currency, the Brazilian real (BRL), has undergone a phase of sustained depreciation against the US dollar (USD) and the euro (EUR). Analysis of average exchange rates reveals a depreciation from approximately R$ 4.90 per dollar at the end of 2023, towards estimates of R$ 5.40 during 2024, reaching R$ 5.50 per dollar in 2025, with forecasts from the Banco Central do Brasil anticipating a further devaluation to R$ 5.60 by 2026.

This currency depreciation strongly incentivises the large agri-food corporations to prioritise the placement of their finished products in overseas markets. Revenue generated in hard currencies (primarily dollars and euros) exponentially maximises corporate profitability once repatriated and converted into the devalued local currency. Simultaneously, Brazil’s domestic socioeconomic landscape is characterised by sustained inflationary pressures, estimated at 4.83% for 2025 and 4.29% for 2026. This is compounded by a formal unemployment rate that, while hovering around 5.8%, conceals a real labour underutilisation rate of 14.4%. This scenario of constrained domestic consumer purchasing power, combined with the uncertainties generated by the recent and historic tax reform approved in the country to simplify the labyrinthine federal and state tax code, severely limits the capacity of the internal market to absorb further production expansions. Consequently, the aggressive channelling of surpluses towards exports is not merely a growth strategy, but a corporate survival imperative.

1.2. Global export performance

Global export volumes have mathematically reflected these structural advantages. In 2024, Brazil’s total chicken meat exports reached a historic record of 5.294 million metric tonnes, generating revenue of approximately USD 9.928 billion, consolidating the country as the undisputed leader in both volume and value. Far from stalling, the sector closed 2025 surpassing its own previous record, with a total exported volume of 5.324 million metric tonnes.

It is worth noting that, while the physical volume shipped increased in 2025, total revenues experienced a very slight contraction of 1.4%, settling at USD 9.790 billion. This discrepancy between rising volume and declining total value is indicative of fluctuations in international commodity prices, intense competitive pressure in the Middle Eastern and Asian markets, and the aforementioned currency depreciation, which enabled Brazilian exporters to strategically reduce their dollar-denominated prices to displace competitors without sacrificing their operating margins in local currency. It is within this framework of hypercompetitiveness, monetary leverage and unrivalled logistical infrastructure that Brazil engages with the European market — a destination that demands the highest quality standards and exceptional regulatory rigour.

2. Quantitative analysis of exports to Europe (2023–2025)

A statistical approach to poultry meat export flows from Brazil to the European continent requires a rigorous analytical distinction between the European Union (EU-27), as a consolidated economic bloc governed by a single tariff and sanitary policy, and the United Kingdom, whose policies and supply chains have diverged substantially since the full implementation of Brexit. Unlike the mass-volume markets in Asia (such as China) or the Middle East (such as Saudi Arabia or the United Arab Emirates), which absorb colossal volumes of frozen whole chicken or generic basic cuts, the European market is characterised by being extraordinarily selective. Exports to Europe are dominated by high-value-added anatomical cuts, processed meat preparations, and salted chicken breasts, designed specifically to integrate into the HRI (Hotels, Restaurants and Institutions) sector and the European secondary food processing industry.

2.1. Volume and value destined for the European Union

nnnnThe trade dynamics between Brazil and the European Union represent one of the most complex agro-industrial flows in the world. By 2023, the consolidation of exports demonstrated the unwavering firmness of the European bloc’s internal demand, even in the face of strict non-tariff barriers. Official government data and ABPA reports converge in indicating that direct sales of poultry meat to the Community market in 2023 totalled approximately 230,300 metric tonnes. This physical volume translated into exceptional profitability, generating revenues of an exact value of 763 million US dollars. The very high price-per-tonne ratio confirms that the export basket towards the EU was overwhelmingly composed of premium cuts and processed products, differentiating itself radically from exports of basic commodities. Complementarily, during this same year, Brazil exported 3,200 tonnes of turkey meat for 15.7 million dollars and 542.8 tonnes of pork for 2.4 million dollars to the same bloc.

nnnnWhen making the analytical transition to the year 2024, customs records indicate that the exported volume maintained notable structural stability, recording a total of 231,900 metric tonnes of poultry meat shipped to European Union ports. The flat maintenance of this volume illustrates a logistical glass ceiling that was not determined by a lack of appetite among European consumers, but rather by regulatory bottlenecks — specifically, the inherited limitation that allowed only 30 processing plants across all of Brazil to export to the bloc —. In terms of value, Brazilian chicken exports to the EU maintained a strong valuation. Although the total annualised figure hovered around 750 million dollars, partial records indicate that, between January and November 2023 alone, exports had already reached 749.2 million dollars for 205,000 tonnes, establishing an extremely high price base that was sustained throughout the entire 2024 cycle.

nnnnThe year 2025 introduced severe epidemiological volatility that disrupted the regular pace of shipments. Between January and September 2025, the cumulative volume of exports to the EU fell to 137,200 tonnes. This temporary contraction was the direct result of precautionary restrictions associated with outbreaks of Highly Pathogenic Avian Influenza (HPAI) in Brazil. However, the final quarter of the year witnessed a monumental recovery. Following the reinstatement of HPAI-free health status, December 2025 recorded an explosive acceleration, with ABPA reporting a 52% increase in volumes exported to the European Union in a single month, boosting the final annualised volume.

nnnnUpon consolidating the accounting close for the 2025 fiscal year, Brazilian inter-ministerial reports indicated that exports of the exclusive sub-heading of “fresh poultry meat” (fresh or chilled unprocessed) alone generated revenues of 592.05 million dollars, representing 6.9% of total global exports for this category and marking an impressive value growth of 18.2% compared to the same sub-heading in 2024. When all tariff categories are aggregated — including salted meats and processed preparations — the total value of the European Union market for Brazilian poultry meat orbited around 762 million dollars, encompassing an estimated total volume of once again 230,000 tonnes. Together with beef, turkey and pork, animal proteins exported by Brazil generated revenues for the country of more than 1.8 billion dollars in 2025 from the EU, encompassing a total of 368,100 tonnes of products.

nnnn| Fiscal Year | Region / Bloc | Exported Volume (Metric Tonnes) | Estimated Total Revenues (USD) | Growth Dynamics |

| 2023 | European Union (EU-27) | 230,300 | $763,000,000 | High-value market stabilisation. |

| 2024 | European Union (EU-27) | 231,900 | ~$750,000,000 | Production ceiling due to plant restrictions (30 facilities). |

| 2025 | European Union (EU-27) | 230,000 | $762,000,000* | HPAI disruption mitigated by 52% increase in December. |

(Analytical note: The total revenue figure for 2025 includes all aggregated tariff sub-headings, of which $592.05 million corresponded strictly to “fresh” chicken, recording an 18.2% increase in that specific category ).

nnnn2.2. The post-Brexit commercial reorientation of the United Kingdom

nnnnThe United Kingdom, operating autonomously outside the umbrella of the European Union’s Common Agricultural Policy (CAP), demands detailed scrutiny. Historically, the United Kingdom has been the second largest supplier of poultry meat to the EU, while simultaneously being one of the largest intra-Community importers. However, since the material execution of Brexit, European imports of poultry meat from the United Kingdom have declined markedly. EU authorities have implemented strict sanitary bans on the importation of chilled minced meat and mechanically separated meat from British territory, while also subjecting UK exporters to burdensome border controls and bureaucratic friction.

nnnnFaced with this gradual isolation and the pressing need to compensate for the structural deficits of its own domestic market — exacerbated by high labour costs that disincentivise intensive domestic processing —, the United Kingdom has profoundly restructured its extra-Community supply chains. Brazil has immediately positioned itself as an indispensable pillar of British food security, especially in the segment of processed and semi-processed products.

nnnnDuring the course of 2025, the United Kingdom imported an astonishing total of 1.7 billion pounds sterling (GBP) in poultry meat preparations at the global level. Of this immense financial flow, Brazil consolidated its position as the third most important country of origin in the world, supplying poultry preparations and processed products to a value of 136 million pounds sterling. In this high-value niche, Brazil competed head-on and was surpassed only by Thailand (685 million GBP) and Poland (281 million GBP).

nnnn| Fiscal Year | Importing Market | Main Import Category | Commercial Value (Pounds Sterling / USD) | Brazil’s Rank as Supplier |

| 2025 | United Kingdom | Poultry Meat Preparations | £136,000,000 GBP | 3rd World Origin |

| 2025 | United Kingdom | Total Meats and Edible Offal | $362,740,000 USD | Top Extra-Community Origin |

The commercial architecture evidenced by the United Kingdom demonstrates a clear strategy on the part of the Brazilian poultry sector: to maximise profit margins by exporting products that require intensive processing. By processing, marinating, salting and cooking the meat within Brazilian plants, exporting companies exploit the asymmetry in labour and energy costs between Brazil and the United Kingdom, exporting the final added value rather than a simple undifferentiated raw material.

nnnn3. The tariff labyrinth and non-tariff circumvention strategies

nnnnThe documented statistics are not the consequence of unrestricted free trade, but rather the result of extremely sophisticated navigation by the Brazilian agro-industry through one of the most protectionist tariff ecosystems on the globe: the European Union. The Brazilian poultry sector faces an intricate network of quotas and tariff-rate systems designed specifically to protect French, German and Polish producers from South American hypercompetitiveness.

nnnn3.1. Tariff Rate Quotas (TRQ) and the salted chicken loophole

nnnnAt present, Brazilian exports are subject to the Tariff Rate Quota (TRQ) system dictated by Regulation (EU) 2020/760. For fresh poultry meat, Brazil holds a preferential quota allowing it to export 15,050 tonnes at a zero percent tariff. However, the penalising barrier is triggered dramatically once this limit is exceeded: surplus volumes are subject to a punitive tariff of 1,024 euros per metric tonne.

nnnnFaced with this tariff wall that would eliminate the commercial margin of any other producer, the Brazilian industry developed a sophisticated legal avoidance strategy: the mass export of salted chicken cuts. By injecting a specific percentage of salt into chicken breast prior to freezing, the product undergoes a metamorphosis in its customs classification, leaving the restrictive fresh meat category and migrating towards tariff codes related to salted meat preparations, which enjoy much broader import quotas and substantially lower tariffs.

nnnn3.2. Commercial geopolitics: the WTO and the Mercosur agreement

nnnnThis tariff engineering has generated constant diplomatic friction. In 2021, the Brazilian government formally escalated the conflict, requesting consultations within the World Trade Organization (WTO) against the European Union. The Brazilian claim argued that the measures imposed by the EU on the importation of meat preparations — specifically salted chicken meat and pepper turkey meat — constituted arbitrary and unjustified barriers. The core of the dispute lay in the food safety criteria applied by the EU regarding Salmonella tolerance limits, which Brazil considered to lack technical-scientific justification, thus constituting blatant discrimination and a violation of the WTO Agreement on the Application of Sanitary and Phytosanitary Measures.

nnnnIn parallel, the legal framework promised a total restructuring with the potential ratification of the Free Trade Agreement between the European Union and Mercosur. Projections announced in September 2025 indicated that this historic pact would introduce a monumental export quota of 180,000 tonnes of poultry meat (carcass weight) at zero tariff exclusively for Mercosur partners (Brazil, Argentina, Paraguay, Uruguay and Bolivia). This quota would be implemented gradually over a six-year transition period, subsequently consolidating as a perpetual annual allocation. Statements by Ricardo Santin, president of ABPA, emphasised that the new quotas would be used primarily to channel Brazilian production, overlapping with the already existing historical quotas. However, the shadow of this treaty provoked an unprecedented defensive reaction within the EU’s agricultural sector, catalysing the events of 2026.

nnnn4. Analysis of geographical nodes and intra-Community price differentials

nnnnThe European bloc is not a homogeneous consumer market; it operates through logistical entry nodes and structurally deficit markets. A deep analysis of intra-regional distribution explains Europe’s existential dependence on products imported from Brazil.

nnnn4.1. The Netherlands: the coronary artery of distribution

nnnnThe Netherlands acts as the unavoidable logistical epicentre and the main gateway for Brazilian chicken into the European continent. Leveraging state-of-the-art port infrastructure such as the Port of Rotterdam, the country functions as an immense “entrepôt”; it imports colossal volumes, carries out value-added processes (such as desalting and packaging), and redistributes the processed goods to final consumer markets in Germany, France, Italy and the rest of the European Union.

nnnnThe pre-eminence of the Netherlands within this ecosystem was mathematically demonstrated during the first four months of 2025. In this short period, Dutch imports from Brazil rose to nearly 200 million dollars, catapulting this European nation to the position of the fifth most important global source of chicken revenue for the Brazilian agribusiness sector. It is critical to analyse the composition of these imports: 55% of the total value transferred corresponded exclusively to salted chicken cuts. This statistic is irrefutable proof that the Brazilian tariff strategy described above is the pillar upon which the trade volume towards Europe rests.

nnnn4.2. Price asymmetries: the Germany, France and Poland triangle

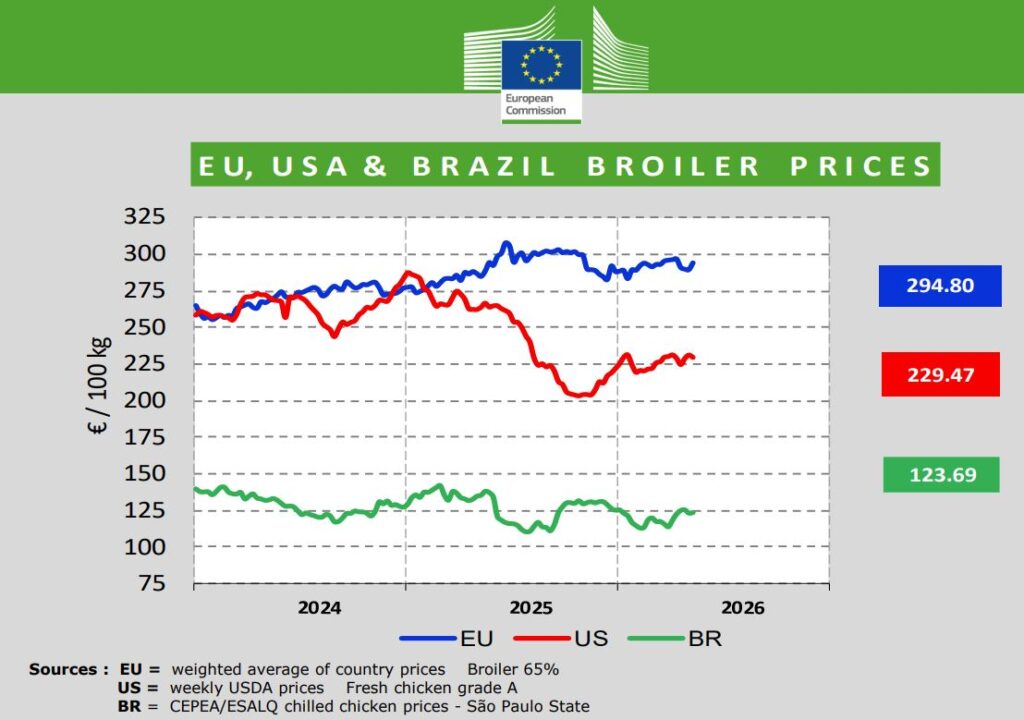

nnnnThe fundamental driver of European demand for Brazilian product lies in the pronounced cost and price asymmetries within Community borders. The European Union presents a scenario of endemic inflation in animal production costs. During 2025, Poland remained the largest domestic poultry producer in the EU, contributing more than 21% of the total Community supply. However, the Polish industry suffered serious setbacks, anticipating a production decline of 3.8% due to devastating Avian Influenza outbreaks in its hatcheries during the first months of the year, compounded by concurrent outbreaks of Newcastle Disease (ND).

nnnnThe shortage of cheap domestic supply exacerbated price differences. European Commission audits revealed that, in 2025, the average retail price of chicken in Germany exceeded that of its Polish neighbour by 2 euros per kilogram (approximately 1.06 dollars per pound). In parallel, the price differential in France was maintained at a premium of 1 euro per kilogram over Poland. These internal price distortions in the major European economies, combined with rising inflation, are forcing operators in the HRI (hotel, restaurant and catering) channel in Germany and France to desperately seek affordable raw materials. Into this vacuum, Brazilian chicken, imported predominantly through the Netherlands, acts as the thermodynamic regulator of European food inflation, mitigating the excess costs that would otherwise fall entirely on the end consumer.

nnnn4.3. The Ukraine disruption and regional triangulation

nnnnThe competitive ecosystem has been profoundly altered by the meteoric rise of Ukraine. Benefiting from temporary tariff exemptions granted by the EU in response to geopolitical considerations, European imports of Ukrainian poultry meat have doubled since 2022. Ukrainian agroindustrial giants, such as MHP, have implemented highly efficient brand perception avoidance strategies.

nnnnMHP not only exports the finished product; the corporation strategically invested in physical processing plants within the borders of the European Union. By using facilities in Slovakia (EU Poultry) located just a few kilometres from the Ukrainian border, trucks transport raw, chilled chicken from Ukrainian slaughterhouses directly to Slovakia. There, the meat undergoes minimal secondary processing and, by exploiting regulatory loopholes, the final product is packaged and marketed under labels that legally designate it as a “processed EU product”. This manoeuvre conceals the Ukrainian origin from the end consumer in Western European supermarkets, silently but aggressively eroding market share in the processed food segment that has traditionally been dominated by frozen meat from Brazil. Furthermore, MHP expanded its influence through the acquisition of the Slovenian/Croatian company Perutnina Ptuj, and the parallel emergence of Petrinja Chicken Company (PCC) announcing investments of 500 million euros in Croatia to produce 150,000 tonnes annually by 2026, consolidates a formidable poultry iron curtain in Eastern Europe.

nnnn5. Epidemiological dynamics: the maze of avian influenza and sanitary barriers

nnnnThe intrinsic competitiveness of the Brazilian industry has been constantly challenged not only by tariff factors, but by the scrutiny of biological controls and global epidemiological crises. The management of Highly Pathogenic Avian Influenza (HPAI) during the period 2023–2025 demonstrates the diplomatic and technical resilience of Brazilian agribusiness.

nnnn5.1. The “HPAI-free” status and the May 2025 crisis

nnnnFor years, Brazil maintained the extraordinary status of being the only major player in poultry trade free of HPAI in commercial flocks, a feat achieved through impenetrable biosecurity barriers. Although the disease was detected in wild and backyard birds in May 2023, the aggressive preventive intervention by the Ministry of Agriculture and Livestock (MAPA) prevented its entry into the commercial chain for two consecutive years. This provided Brazil with an insurmountable advantage over the United States and the EU, both of which lost tens of millions of birds through preventive culling and suffered consequent international export embargoes.

nnnnHowever, the shield of invulnerability collapsed in May 2025. Health authorities confirmed the first outbreak of Highly Pathogenic Avian Influenza in a commercial poultry facility located in the municipality of Montenegro, in the state of Rio Grande do Sul. The international repercussions were immediate; numerous trading partners activated contingency protocols and temporarily suspended imports of Brazilian meat. Japan, the second largest global buyer of Brazilian chicken (having imported 443,000 tonnes in 2024), led the partial blockades, followed by Middle Eastern nations and major Asian markets. The European Union issued coordinated suspensions, threatening to irreversibly divert trade flows towards other suppliers.

nnnn5.2. Veterinary diplomacy: the effectiveness of regionalisation

nnnnTotal economic catastrophe was avoided thanks to the meticulous diplomatic architecture previously established by Brazil: sanitary “regionalisation” protocols. Under the regulations of the World Organisation for Animal Health (WOAH), Brazil demonstrably proved its capacity to isolate, trace and eradicate the outbreak without contamination spreading beyond the affected municipality. Rather than bearing a blanket national embargo that would have paralysed exports from key states such as Paraná or Santa Catarina, Brazil confined the impact to micro-local restrictions.

nnnnThe technical execution was impeccable. After fulfilling the international requirement of 28 consecutive days with no detection of new cases within the observation perimeter from the suppression of the original outbreak in Rio Grande do Sul, WOAH officially validated the country’s epidemiological update. In a historic statement on 18 June 2025, the Brazilian State solemnly declared the country once again free of HPAI. Importing nations began to lift their embargoes gradually. The outcome with Europe arrived on 4 September 2025, when European Union authorities formally announced that they recognised the restoration of Brazil’s HPAI-free status and proceeded to open their customs markets fully and gradually to Brazilian poultry exports. It was this crucial restoration of market access in September that unleashed the export avalanche at the end of the year, crystallising in the astonishing year-on-year increase of 52% in shipments sent to the EU in December 2025, offsetting almost entirely the losses of the second and third quarters.

nnnn5.3. Operation “Carne Fraca” and the restoration of “pre-listing”

nnnnSimultaneously with the management of the viral crisis, 2025 witnessed the final redemption of a regulatory conflict that had strangled the poultry sector for nearly five years. Between 2017 and 2018, the devastating police operation “Carne Fraca” exposed systemic networks of fraud, manipulation of hygiene certifications and widespread bureaucratic corruption within multiple beef and poultry processing plants across Brazilian territory. The European Union’s response was swift and punitive: it unilaterally suspended the “pre-listing” model. This model was the cornerstone of logistical agility; it allowed the Brazilian government to autonomously certify and approve which cold-storage facilities met Community standards without the need for prior on-site bureaucratic inspections by European officials.

nnnnThe suspension of pre-listing resulted in a monumental bottleneck. The export infrastructure was reduced and paralysed, strictly limiting exports of poultry meat to the bloc to only 30 pre-authorised processing plants. The impact was evident in total volumes: whereas in the golden years prior to 2017 Brazil consistently managed to export more than 500,000 tonnes annually to the European market, following the sanctions the figure collapsed and stagnated mechanically around the structural limit of 230,000 tonnes per year observed in 2023, 2024 and 2025.

nnnnFollowing exhaustive internal reforms and transparent demonstrations of compliance, the European Commission dispatched auditors from its Directorate-General for Health and Food Safety (DG Sante) at the end of 2023. The results confirmed that Brazil had successfully remedied all the methodological and procedural deficiencies inherited from the previous decade. The culmination of this lengthy process came in the last quarter of 2025, when Brazil’s Ministry of Agriculture and Livestock (MAPA), following high-level meetings with EU officials (including Trade Secretary Luis Rua and European negotiator Christophe Hansen), joyfully announced the official resumption of the pre-listing system for the export of chicken, turkey and duck. Ricardo Santin, representing ABPA, highlighted that this ruling validated the unquestionable solidity of the national sanitary system, granting Brazilian corporations enormous financial predictability and clearing the way for dozens of new meat plants to flood the European market with protein in the years ahead.

nnnnThe scenario at the end of 2025 projected an era of unprecedented exponential growth for Brazil in the Old Continent. However, this optimism would abruptly disintegrate just a few months later.

nnn

6. The geopolitical fracture of 2026: antimicrobial regulation as a definitive barrier

nnnnThe expectations of an overwhelming resurgence of Brazilian exports to Europe collided head-on with an unprecedented legislative wall in early 2026. The trade dynamic, which until that point had revolved around tariffs, quotas and viral pathogens, mutated into an open conflict over intensive farming practices and pharmacological resistance.

nnnnn6.1. The May decision and the September ultimatum

nnnnOn 12 May 2026, a shockwave swept through the corridors of agroindustrial power in São Paulo and Brasília: the European Commission formally published an update to its master list of third countries authorised to export products of animal origin to the Community bloc, ruling, to widespread astonishment, the categorical exclusion of Brazil.

nnnnThe grounds put forward by the Brussels authorities were not based on fraud incidents or avian pathogen outbreaks, but on non-compliance with cutting-edge veterinary regulations: the systemic inability of the Brazilian productive apparatus to provide irrefutable guarantees regarding the non-use and strict traceability of antimicrobial compounds in the rearing of livestock and poultry. Eva Hrncirova, spokesperson for the European Commission in the area of Health, made it unequivocally clear that, in order to regain commercial access, the Brazilian State would need to demonstrate the implementation of infallible audit mechanisms guaranteeing that no animal whose derived product reached European tables had been treated with antibiotics as growth promoters throughout its entire life cycle.

nnnnThe time dimension of the sanction intensified the severity of the crisis. The European Union set an unappealable deadline of 3 September 2026. From that date, all trade restrictions and embargoes on meat, eggs and products of animal origin would enter into full force, plunging export supply chains into immediate logistical paralysis if the required technical compliance dossiers were not submitted.

nnnn6.2. The macroeconomic damage quantified

nnnnThe scale of value destruction resulting from the effective implementation of this exclusion is without precedent in the recent history of bilateral relations. Extrapolating the consolidated metrics from fiscal year 2025, the embargo would completely dismantle a commercial market that generates approximately 1.8 billion dollars annually in animal protein export revenues for Brazil’s trade balance (equivalent to around 10 billion Brazilian reais, depending on exchange rate fluctuations). In volumetric terms, more than 368,100 tonnes of food per year would be blocked at ports.

nnnnWhile beef heads the list of affected products (representing revenues of over 1.048 billion dollars and covering 128,000 tonnes), the damage to the poultry sector is equally devastating. The Community exclusion would wipe out the trade in chicken meat which, as demonstrated in 2025, generated revenues for Brazil of 762 million dollars (with 230,000 tonnes exported). Complementary and niche sub-segments, such as turkey exports (valued at 15.7 million dollars for over 3,200 tonnes) and even the limited but emerging pork exports (2.4 million dollars and 542 tonnes) would be collaterally erased from the European commercial map.

nnnn6.3. Geopolitical analysis: the instrumentalisation of the Mercosur agreement

nnnnThe joint statement issued by the Ministries of Agriculture, Development, Industry and Foreign Affairs of the Government of Brazil expressed profound consternation and a firm rejection, describing the exclusion as an unexpected “surprise” and emphatically defending the proven operational excellence of its productive apparatus, which has guaranteed the safe and uninterrupted supply of food to Europe for more than forty years.

nnnnHowever, behind the technical rhetoric of antimicrobials lies a geopolitical chess game of monumental proportions linked to the controversial and stalled Free Trade Agreement between the European Union and Mercosur. The trade agreement postulates the historic elimination of tariffs and the creation of the aforementioned mega-import quota of 180,000 tonnes of tariff-free chicken meat from South America. This has deeply enraged coalitions of poultry farmers and livestock producers in nations such as Spain, France, Italy, Poland, etc., who vehemently argue that the agreement would destroy their livelihoods by forcing them to compete against South American multinationals that are not subject to the same punitive regulations on animal welfare, animal health and sanitary standards, or the use of antibiotics as growth promoters — the latter having been totally prohibited in the EU for decades, among other measures.

nnnnWithin this analytical framework, the political decision by Brussels to strictly enforce standards on the use of antimicrobials — conceptually aligned with the “Farm to Fork” policy of the European Green Deal — operates de facto as a powerful non-tariff barrier. By systematically disqualifying Brazil and placing upon it the burden of proof regarding the segregation of its supply chain, the European Commission achieves a dual objective: firstly, to appease the anger of European poultry farmers and livestock producers by demonstrating that it will strictly enforce European regulations on all imports; and secondly, to effectively neutralise the imminent trade facilitations that would derive from the ratification of the Mercosur Treaty.

nnnn7. Structural reconfiguration and strategic outlook towards 2034

nnnnThe collision of forces between Brazil’s unlimited productive efficiency and Europe’s regulatory complexity generates ramifications that will reverberate throughout the entire next decade in global commodity markets.

nnnnThe joint macroeconomic projections drawn up by the Organisation for Economic Co-operation and Development (OECD) and the Food and Agriculture Organization of the United Nations (FAO) in their report “Agricultural Outlook 2025-2034” underline that global demand for chicken meat will continue its inexorable growth, far outpacing beef and pork due to its versatility, feed conversion efficiency and general perception of affordability among low- and middle-income consumers.

nnnnWithin this forward-looking horizon (2025–2034), analytical models predict that Brazil will continue to expand its global supremacy at a rate above the world average, incorporating an estimated additional volume of 512,000 tonnes of poultry meat by 2034, representing nearly 40% of the total 1.293 million metric tonnes of absolute global growth forecast for that timeframe. This expansion will be underpinned by the relentless growth of aggregate demand in dynamic and hyperconnected economies such as the United Arab Emirates, Saudi Arabia, Mexico and the countries of Southeast Asia, which have demonstrated a propensity to prioritise supply security and price stability over the regulatory rigour that characterises the European Union.

nnnnIn the short and medium term, the Brazilian poultry sector faces an existential dilemma with regard to the European market. To avoid the total disintegration of its European revenues before the September 2026 deadline, the industry will need to undertake a pharaonic technical overhaul. This will require the accelerated implementation of fully segregated production lines, audited via blockchain technology or equivalent traceability systems, certifying from the birth of the bird to its final processing the complete absence of antimicrobial growth promoters. If the logistical magnitude of this technical requirement proves unachievable within the stipulated timeframe, Brazil would be forced to suddenly redirect a surplus of close to 230,000 tonnes of premium cuts towards other geographies, causing a collateral deflationary impact on international poultry protein prices.

nnnnFor its part, Europe’s paradox will deepen irreversibly. Self-imposedly isolated from the world’s cheapest supplier through its antimicrobial regulations, permanently unable to import from the United States due to its pathogen reduction regulations (chlorine-washed chicken), and facing the geopolitical tensions arising from the influx of Ukrainian chicken, or Chinese chicken, among others, which threatens its fragile internal political cohesion, the European consumer will bear the full final cost of the EU’s regulatory framework. A regulatory “corpus” which, it must not be forgotten, is the strictest in the world in matters of animal welfare and animal health, and in food safety for the population.

nnnnnnnnnnnnnnnn

To find out more:

nnnn-. EU-MERCOSUR Agreement

-. EU-MERCOSUR Agreement impact on Poultry. Report by AVEC-COGAG. 20250624

-. The “safeguard clause“: a false protection, pure window dressing

nnnn

Do you want to stay one step ahead in poultry?

Subscribe for free to our eNewsletter and receive a weekly selection

of the best information to anticipate trends, stay up to date and grow as a poultry professional.

NeXusAvicultura: Vision, Insight, Quality and Context.